Updated with 2025 promo details. Pennsylvania State Employees Credit Union (PSECU) has a $300 new checking account bonus. That is also my referral link as I successfully did a similar $300 deal previously. PSECU is a digital-first credit union with a very open membership. If you don’t satisfy the available free options, anyone can join with $10:

Don’t meet any of the criteria above? No problem! You can still become eligible for PSECU membership by joining the Pennsylvania Recreation and Park Society (PRPS).

PRPS is a statewide association providing education, advocacy, and resources for those working and volunteering to manage Pennsylvania’s 6,000+ local parks. Park and recreation departments provide safe and affordable recreation opportunities, creating stronger and more inclusive communities.

PRPS membership dues are $20, but we cover $10 when you select to join PRPS during our application process.

There may also be a required $5 initial deposit into a share savings account. I also experienced a hard credit check on Experian when I joined over a year ago, but more recent reports are that they have switched to a soft pull. Here are the details on the bonus requirements:

$300 Checking Bonus Requirements

- Become a PSECU member using promo link and promo code 300REFER (should be automatically applied) and be approved for at least one savings and one checking account with debit card.

- Sign up and log into digital banking (online or mobile).

- Set up and receive 2 Qualifying Payroll Direct Deposit(s), each of $500 or more, into either the new savings or checking accounts.

- Above must be completed within 100 days of establishing your membership.

My application process went smoothly and similar to other credit unions. I did have to upload a scan of the front and back of my driver’s license to help verify my identity (which is a good thing in my opinion) as well as answer some identity verification questions based on my credit report. The application took a couple days to process but I was able to get my account information and online access without any phone call or paperwork required. I did have to call them briefly to get my checking account number (didn’t want to wait on the free checks to arrive) in order to set up my direct deposit. My bonus arrived without issue and as promised.

One bonus per tax ID, so a couple could each open their own PSECU accounts and get $300 each even if they live in the same household.

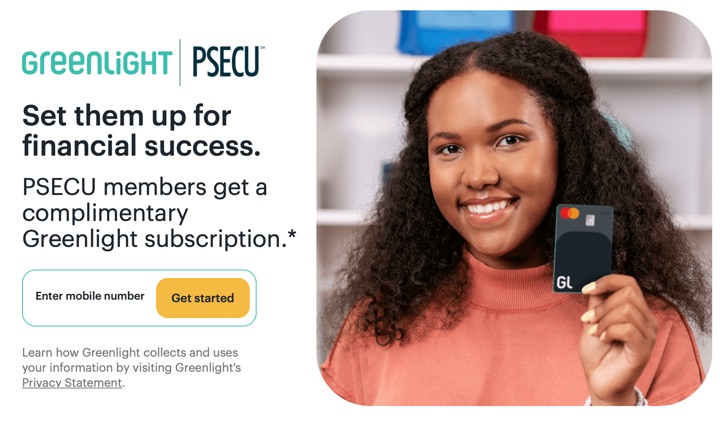

Greenlight perk. Another useful perk of PSECU for those with kids and teens is they include a free Greenlight subscription, which is a popular reloadable debit card service for kids. This is usually $5 a month ($60 a year). Here’s my Greenlight Kids Debit Card review.

More fine print:

$300 New Member Bonus Terms and Conditions

From 1.1.25 to 12.31.25, PSECU is running a new member incentive bonus. To receive $300, new members must sign up with promotional code 300REFER and satisfy each of the requirements listed below. After the first 100 days from establishing membership, your status to receive the bonus will be assessed and processed, which can take up to 45 days. This means, if all requirements are met, you can expect your bonus to be deposited into your Regular savings share within 145 days from establishing membership. Promotion open to U.S. Residents who are 18 years of age or older at the time membership is established. Limit one (1) new member $300 New Member Bonus per tax identification number used to open a new PSECU account. Joint owners listed on accounts are not eligible to be rewarded for this bonus unless they open their own account. You will not be eligible for the $300 New Member Bonus if you are a current PSECU member, have closed an account within the past 12 months, or have received any new member incentive bonus within the past 12 months.

Qualifying Payroll Direct Deposits are defined as paychecks, Social Security payments, and pension payment.

The following are not Qualifying Direct Deposits: person to person transfers (P2P), demand deposit account to demand deposit account transfers (for example, from a checking account to another checking account), and deposits or ACH transfers not from an employer or the government (for example, online transfers or bank transfers).

Sam’s Club has a new discount offer on new memberships. This is slightly cheaper than the previous

Sam’s Club has a new discount offer on new memberships. This is slightly cheaper than the previous

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)